- Withholding can be useful as you get older

- For distributions with less than $1000 tax impact, it may be smarter not to withhold.

- For Roth conversions, in most cases it is better not to withhold taxes, especially if you are not 59.5 yet.

You are retired and are planning to withdraw some of your tax-deferred money from your traditional IRA or 401k. As you click through the screens, there is a message about withholding taxes. Should you withhold taxes or decline to do so?

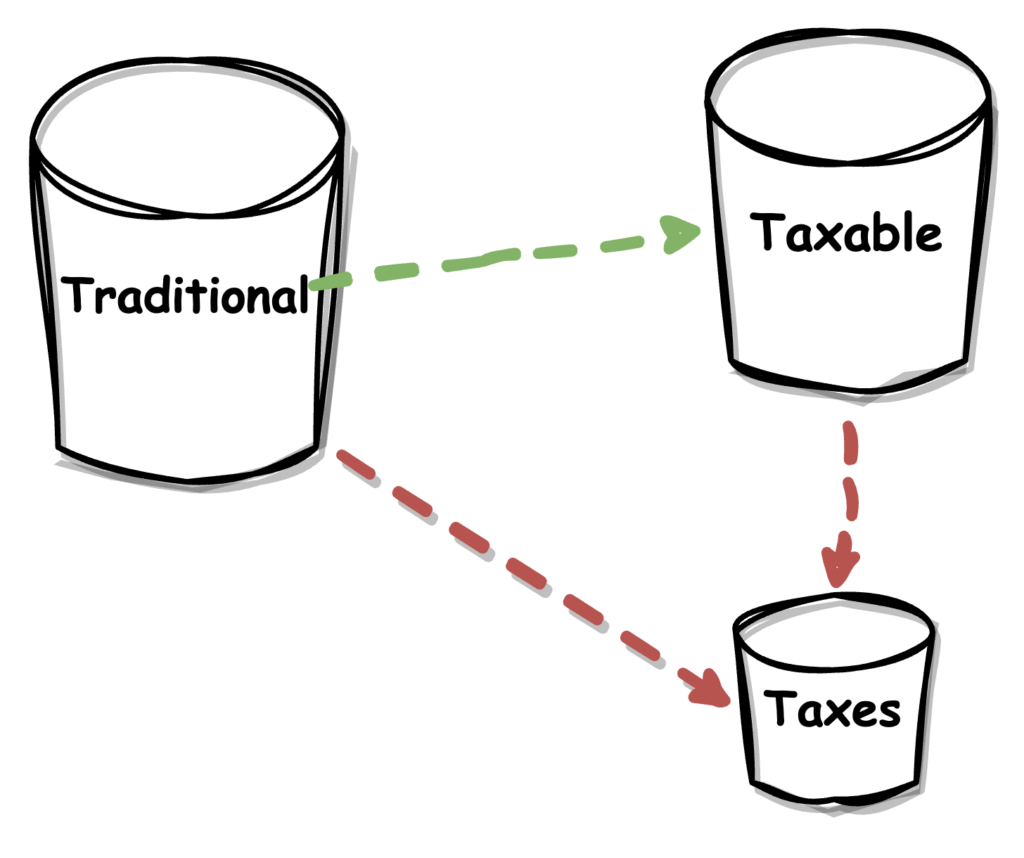

As the math turns out, it depends on the amount and the intended use of the funds to be withdrawn. If you are doing a Roth conversion, that is, rolling over the IRA funds into the Roth IRA, then it is better not to withhold taxes and instead pay taxes from the taxable account. In fact, if you are under age 59.5, you definitely do not want to withhold taxes from your traditional IRA. If you are distributing the money into your taxable account for spending needs, then it’s a bit of a toss-up, but when in doubt, you should withhold taxes. We’ll consider a couple of different situations below. For both situations, let’s assume that John is above age 59.5 and that he has met any five year rules for Roth IRAs to avoid any early withdrawal penalties.

Situation 1: IRA Distribution for Spending Needs

In this case, John wants to spend $9,000 from his traditional IRA to fund a once-in-a-lifetime luxury cruise to cross it off of his bucket list. If he is in the 10% tax bracket, he will need to actually process a withdrawal of $10,000 from his IRA. He can either withhold the $1000 ahead of time or withdraw the entire amount and pay the $1000 from his taxable account later. The optimizing approach would indicate that if you held on to your $1000 longer before paying taxes, you would be incrementally better off. However, keep in mind that the IRS has rules regarding the timing of estimated tax payments, and depending on the amount of taxes, John potentially could owe underpayment penalties at tax return time.

Of course, in this example with $1000 taxes owed, John likely may already withhold enough based on the safe harbor rules. Assuming a 5% interest rate, John could potentially save an extra $45 ($50 interest – 10% taxes) by waiting to pay taxes. On the flip side, is this something that John would want to worry about? It’s probably not worth it if John’s tax owed at tax return time is higher than $1000, because of the way the IRS calculates underpayment penalty. Regardless, there isn’t an answer that is always correct in this scenario. It is ultimately up to the taxpayer, but generally as you get up in the years, you’re likely to opt for convenience by withholding taxes rather than go for optimizing every cent. And that’s perfectly okay.

Situation 2: Roth Conversion

In this situation, John wants to do a Roth conversion of $20,000 from his traditional IRA while he is in the 12% bracket, and let’s assume that he can stay under the 22% even after the conversion. Taxes on the $20,000 are going to be $2,400. He has the choice to pay this tax by either withholding taxes and converting $17,600 into the Roth IRA, or by converting the entire $20,000 and paying taxes from his taxable account. Let’s assume that he had $50,000 in his traditional IRA and $10,000 in his taxable account before this Roth conversion. Let’s see how his account balances end up afterwards.

Option A: Withhold Taxes

– Traditional IRA: $50,000 –> $30,000

– Roth IRA: $0 –> $17,600

– Taxable: $10,000 -> $10,000

Total: $30k + $17.6k + $10k = $57.6k

Option B: Don’t Withhold; Pay Taxes Later:

– Traditional IRA: $50,000 –> $30,000

– Roth IRA: $0 –> $20,000

– Taxable: $10,000 -> $7,600

Total: $30k + $20k + $7.6k = $57.6k

As you can see, the resulting amount is the same when looking at the overall dollar amounts. But, the difference is that now with Option B, you have ended up with a greater Roth IRA, which you can later withdraw at any point in time.

One key pitfall that needs to be mentioned: If you are not age 59.5 yet, either because you are an early retiree or because you happened to get stuck with pro rata taxes on Roth conversions while doing a backdoor Roth IRA, withholding taxes from your traditional IRA is actually a recipe for a 10% penalty mini-disaster. That is because, when you withhold taxes on a Roth conversion, the taxes get sent right to the IRS, but the IRS has no way of knowing that this was part of a Roth conversion. So, it simply treats the withholding as a distribution from the traditional IRA, and therefore subject to a 10% penalty tax for early withdrawal. To avoid this trap, you will want to never withhold on a Roth conversion if you are under age 59.5.

Otherwise, the choice comes down to whether you want to keep more in Roth IRA vs Taxable. In most cases, the Roth IRA will beat out the Taxable account in terms of desirability. If you have regular cash flow coming in to the taxable account, such as Social Security benefits or pensions, then using those taxable funds to pay taxes is smart. But, if you only have very large capital gain positions that you do not want to liquidate, and are wanting to leave the taxable account for the benefit of your heirs, this begins to resemble Situation 1 above.

The relatively small examples above may not seem particularly impactful either way. But if you are in higher tax brackets and you have accumulated significant funds in the traditional pretax account, you will definitely want to understand whether withholding is better or not. Please feel free to contact us for an analysis specific to your situation.